Know These Things Before Filing A Roof Claim!

Understanding your insurance policy and knowing your deductible before filing a claim for damage to your roof is very important. A deductible is the amount of money you are responsible for paying out of pocket before your insurance company starts covering the costs associated with a roofing claim. Learn about Georgia insurance deductibles legislation, the various ways insurance companies pay out a claims, factors impacting your total out of pocket obligation, and more.

How Insurance Companies Pay Roofing Claims

What Is a Roofing Deductible?

A roofing deductible is the amount of money you need to pay out of pocket before your insurance starts covering the costs of a roofing claim. It acts as a form of self-insurance, ensuring that you share a portion of the financial responsibility for repairing or replacing your roof in the event of damage. Georgia law requires homeowners to pay their deductibles, and has prohibited contractors from “absorbing” deductibles for a little over a decade. Unfortunately, that still does not stop shady contractors from knowingly committing fraud. For example, if an insurance company provides an estimate and scope of work to a homeowner for $10,000, some contractors will charge the homeowner $9,000, but still submit an invoice to the homeowner’s insurance company stating they charged $10,000, thus “absorbing the cost” of a $1,000 deductible.

In some cases, homeowners still ask us to provide them an estimate despite insurance already providing them with their own estimate. When this happens, we let them know that if our price is lower, their insurance company will simply match our price and will not give them a couple thousand extra dollars just because they’re nice guys 🙂 You can read more about that

here from a 2018 bulletin released by a former Georgia Insurance Commissioner.

Understanding Claim Payouts

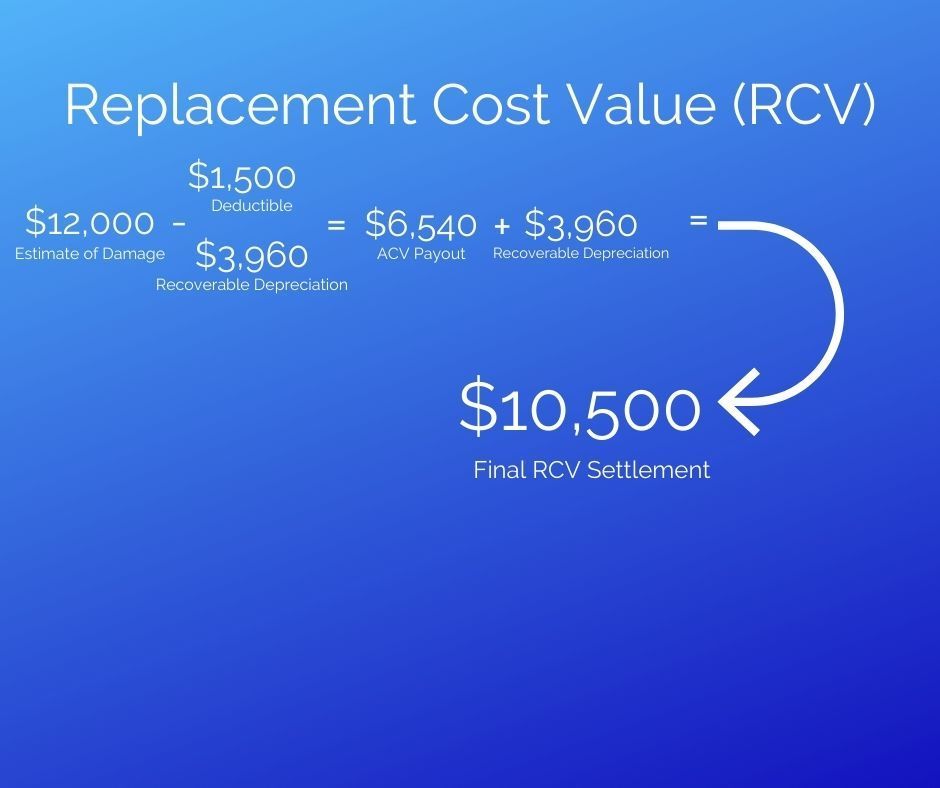

RCV (Replacement Cost Value):

In Georgia, RCV policies are the most common. They fully reimburse the cost of roof repair or replacement without accounting for depreciation. Regardless of the roof’s age or condition, the insurance company covers the actual replacement cost with similar quality materials. Market prices for labor and materials determine the appropriate payout. Policyholders pay the specified deductible before insurance coverage begins. RCV policies offer extensive coverage, disregarding wear and tear or the roof’s age. Typically, the homeowner’s deductible is the only out-of-pocket expense. Contractors typically collect that ACV check as well as the deductible before the roof install. After the work is completed, you or your contractor will then send the insurance company the Certificate of Completion and the insurance company then releases the final depreciation check.

Below is an example of an RCV claim payout:

- Total estimate: $12,000

- Homeowner’s deductible: $1,500

- Insurance company depreciation of the roof: $3,960

- ACV/1st check from insurance: $6,540

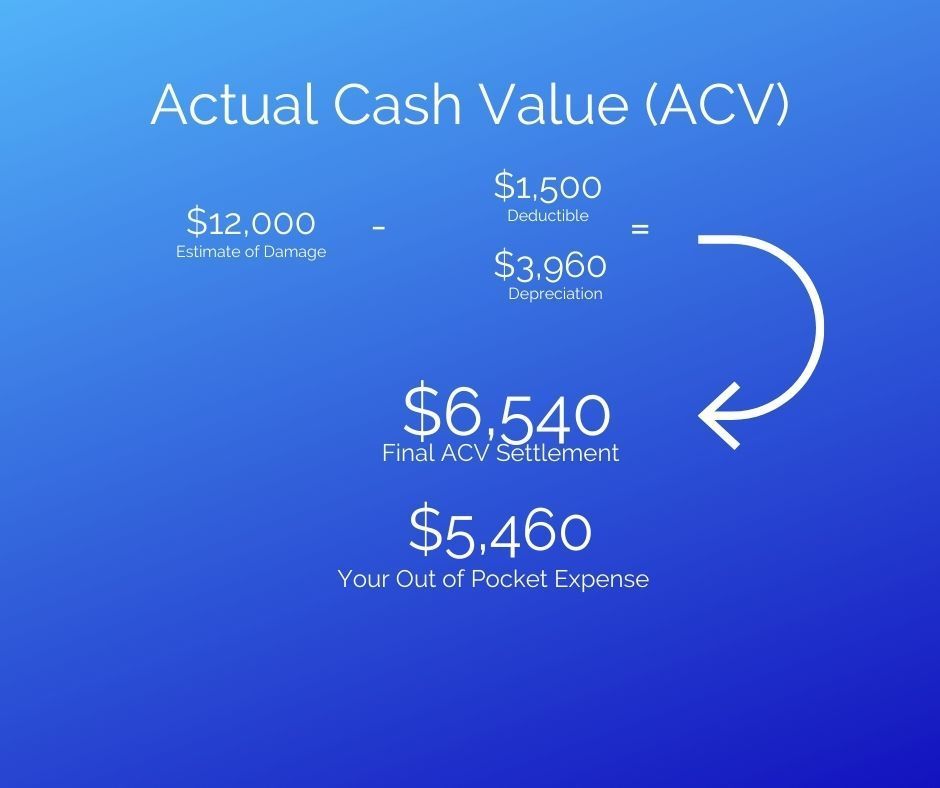

ACV (Actual Cash Value)

Another type of insurance policy growing in popularity with some carriers is called an ACV (Actual Cash Value) only policy. An ACV policy is a type of coverage that takes into account the depreciated value of your roof when determining the amount the insurance company will pay for a claim. Under this policy, the insurance company considers factors such as the age and condition of your roof at the time of the claim. The payout you receive for roof repairs or replacement is based on the depreciated value rather than the full replacement cost. As a policyholder, you are responsible for paying the deductible based on the depreciated value. This type of policy typically results in a lower payout compared to policies that offer full replacement cost coverage (RCV), where the insurance company covers the cost to replace the roof without factoring in depreciation.

In the image below we will look at the same numbers as the RCV example. The total estimate is still $12,000, the homeowner’s deductible remains at $1,500, the insurance company depreciates the roof the same amount at $3,960, which makes the 1st check from insurance equal $6,540. However, the $6,540 paid out by insurance is typically the only check a homeowner will receive from insurance, and the homeowner is responsible for the rest of the funds. This may seem like a bad policy, but for those looking to keep their monthly budget as low as possible, ACV policy’s come with much lower premiums than their traditional RCV counterpart.

Navigating Roofing Insurance Claims

There are other types of insurance policies, but the two we read about today are the most common seen in Georgia. Understanding your insurance policy and the concept of roofing deductibles is crucial before filing a claim for roof damage. Always remember that Georgia law requires homeowners to pay their deductibles, preventing contractors from “absorbing” these costs and that it’s important to be aware of potential fraudulent practices by contractors. The only way you will not have an out of pocket expense is if insurance covers a peril and you choose to not get that particular work done. For example, insurance pays for your gutters to be replaced do to hail damage, but rather than getting them replaced you choose to utilize the ACV portion of those funds to offset some of your out of pocket costs. Keep in mind that if you do that, you and/or your contractor cannot ask to recoup the depreciation funds for those gutters.

Conclusion: Informed Decisions for Roofing Insurance Claims

In summary, when it comes to insurance claim payouts, RCV (Replacement Cost Value) policies provide greater coverage, reimbursing the full cost of repairing or replacing your roof without factoring in depreciation. On the other hand, ACV (Actual Cash Value) policies consider the depreciated value of your roof, resulting in lower payouts. While ACV policies may have lower premiums, they require homeowners to cover the remaining funds beyond the insurance payout. Understanding these aspects empowers homeowners to make informed decisions regarding their roofing insurance claims.

Our team at NBS Roofing would be happy to answer any questions you have about this topic and more! Call or text us today at 470-729-0678!

Book Your Free Roof Consultation

Have a question? We’re here to help! Send us a message and we’ll get be in touch.